Laser Eyes Don't Help!

.....If Bitcoin Mass Adoption is the Goal

Admittedly, Bitcoiners can be a pretty strange crowd. And brazen. Especially on Twitter. And yes, sometimes downright rude.

Many of them use a lot of profanity. They rail at people who buy other crypto coins, referring to them as “Shitcoiners.” One really famous podcaster used to open his episodes by saying the goal of Bitcoiners was “motherf___ing mass adoption.”

One commonly used mantra of the hardcore Bitcoiners, when assailing non-Bitcoiners is, “Have fun staying poor.” Yikes. Brutal. This can be used against alt-coiners and no-coiners alike.

The favorite hobby of many of the best-known Bitcoin advocates is trolling on Peter Schiff. Schiff is the CEO at Euro Pacific Precious Metals and as such is a big proponent of buying gold in people’s portfolios. Bitcoiners have changed their portfolio pics to Schiff’s likeness, or set up framed pictures of Schiff in their offices. They constantly put up charts, comparing gold’s performance to Bitcoin’s. They’ve also, naturally, instructed Peter to “have fun staying poor.” Schiff gives it right back:

They easiest way to recognize the Twitter profile of the OG Bitcoiner, however, is to spot the “Laser Eyes” emblazoned on their profile pictures. This originated several months ago as Bitcoiners boldly proclaimed, “laser rays until $100K.” Several celebrities and athletes followed suit - Paris Hilton, Elon Musk, Cameron and Tyler Winklevoss, and La La Anthony, to name a few. Even Senator Cynthia Lummis from Wyoming showed her support with the Laser Eyes, and just this week, football legend Tom Brady followed suit.

Peter L. Brandt, CEO of trading firm Factor, LLC, appeared on Laura Shin’s popular podcast “Unchained” last month. He espoused many of the same feelings I have about the actions of Bitcoiners. He believes the Laser Eyes, the “over enthusiasm,” and the “chest pounding” are signs that the markets have gotten a bit frothy, and are a very bearish factor for Bitcoin. And they do nothing to promote mass adoption. That’s key.

Look, I think Twitter should be fun. I think Bitcoin is an exciting new technology. I think it can be digital gold, gold 2.0. The possibilities are really exciting. I also know that the earliest Bitcoiners were a revolutionary type crowd, anarchists and libertarians. They were rebelling against the traditional financial system, right after the Great Financial Collapse. Remember Occupy Wall Street? Hey, you want to make an omelet, you gotta break a few eggs, right?

The problem, as I see it, is this. When you’re trying to revolutionize the legacy financial world, you need mass support. You can’t piss too many people off. You seek government blessing. You can’t perpetuate the notion that Bitcoin is the currency of criminals. (See last week’s newsletter!) The Bitcoin movement needs to be serious, to show the effectiveness of a great, new technology. There are thousands of bright, talented people doing great things in the crypto space. They need to do it the right way, and Bitcoiners at all levels should be mindful of what is needed to achieve that goal of mass adoption. And, the Laser Eyes aren’t helping. Even with Paris Hilton on the team.

(By the way, gold has a place in portfolios. It’s not Bitcoin or gold. Can’t we get along?)

What Ever Happened to the Libra Coin?

It was June 18, 2019. Facebook, the social media behemoth, rocked the tech world and announced plans to release its own cryptocurrency and payment network. Originally dubbed “Libra,” the plan had been in the works since at least February of 2018, so the rumors were out there. Several other companies were involved in the founding of the Libra Association, including eBay, PayPal, Visa, Mastercard and Stripe.

It was an ambitious plan.

The goal of the Libra founders was to create a global digital currency that would promote financial inclusion to the unbanked around the world. The Libra coin was to be a stablecoin that represented a basket of currencies, including the US dollar, the Euro, and the British pound. The term “Libra” came from a term in ancient Rome that represented a unit of weight. It was also given its own symbol, similar to the dollar sign: ≋.

Blockchain, not Bitcoin

The currency was planned to be created on a blockchain application, of course, but was not intended to be a totally decentralized platform like Bitcoin. The network was to rely on trust in the Libra Association, as the currency’s de facto central banker. The Libra blockchain was designed to handle 1,500 transactions per second, which would be exponentially faster than the blockchains of Bitcoin or Ethereum.

The wallet that would store the Libra coins was called “Calibra,” and would be accessible through Facebook Messenger, WhatsApp, and a standalone Libra app. From there, users would be able to load funds into Libra, send funds to friends, or pay merchants. The applications sound similar to PayPal or Venmo transactions, but the currency would be this new coin, the Libra.

Not So Fast!

Libra was immediately greeted with regulatory concerns. Within minutes of the announcement, French Finance Minister Bruno Le Maire stated that Libra could not be allowed to become a sovereign currency. He promptly warned the French Parliament about his concerns over possible money laundering and privacy concerns, as well as potential financing of terrorist activities.

It took the United States a couple of hours. (These responses had to have been “in the can.”) Congresswoman Maxine Waters, the chairperson of the House Financial Services Committee, immediately asked Facebook to halt the launch of Libra. Fed Chairman Jerome Powell testified before congress just three weeks later, citing “serious concerns” over how Libra would deal with money laundering and other issues. President Trump weighed in as well, suggesting that crypto developers like Facebook should probably be required to apply for a federal banking charter. Whoa.

Just three months after the June announcement, Facebook CEO Mark Zuckerberg said that Libra would not launch anywhere in the world without first obtaining the approval of US regulators. Then, just one month later, sensing the difficult path to regulatory approval, several big players withdrew from the Libra Association. They included PayPal, eBay, Visa, MasterCard and Stripe.

Where Are We Now?

After regrouping in 2020, Facebook announced that the Libra coin would be a stablecoin pegged to the US dollar, rather than to a basket of currencies. Not nearly as ambitious as the original plan. In December of 2020, the project was rebranded as “Diem,” the Latin term meaning “day.” The association was also renamed the “Diem Association.” It currently has 27 members, including Coinbase, Lyft, Uber, Shopify, and naturally, Facebook.

Last month, the Association announced that it still had plans to release the Diem coin in 2021. Stay tuned.

Book Review of the Month:

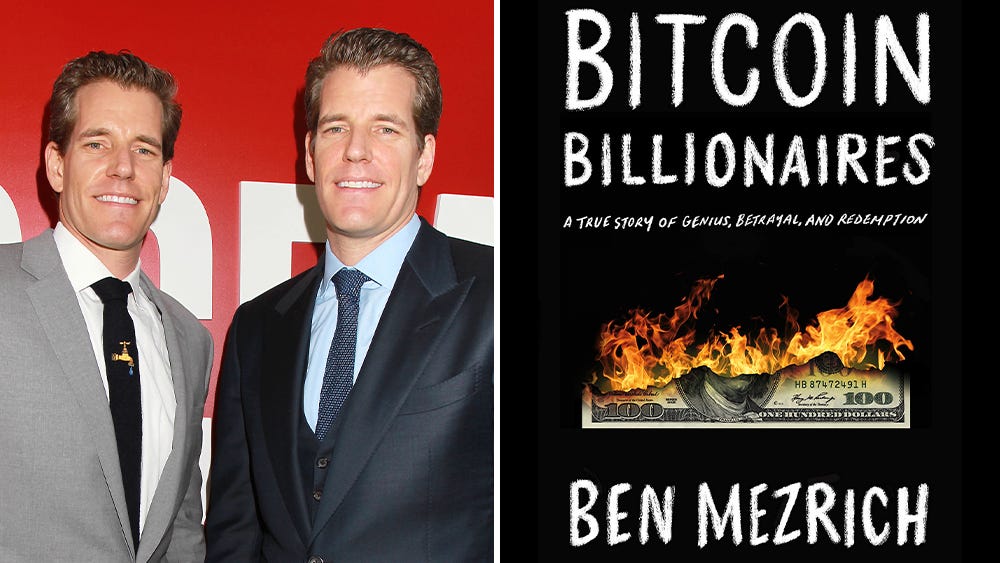

Bitcoin Billionaires, by Ben Mezrich. Publ. May 2019, 279 pages, Flatiron Books.

“It’s either the next big thing or total bullshit.”

Those were the words of Cameron and Tyler Winklevoss when they first learned about Bitcoin, in 2012. On vacation on the island of Ibiza, of all places. But let’s back up a few years.

These are the Winklevoss twins that became household names following the movie “The Social Network,” and the book, also by Mezrich, “The Accidental Billionaires.” Published in 2009, Mezrich’s bestseller told the fascinating story of the founding of Facebook and of the twins’ very public battle with Mark Zuckerberg. Harvard-educated and Olympic rowers, the Winklevii, as they’ve come to be known, at first were inclined to let Zuck have his start-up venture. They famously stated that “men of Harvard” wouldn’t file lawsuits against schoolmates. They would reconsider.

Following a long legal battle and eventual settlement, the twins found themselves with upwards of $50 million and were looking for something to do with it. They attempted to start a venture capital firm, but found that no one in Silicon Valley would have anything to do with them following the Facebook/Zuckerberg battle. This is where the book really gets good.

Second Act

On the Ibiza vacation, the twins meet an eccentric character who starts explaining the world of “cryptocurrencies” to them. After consuming, in their words, “a bunch of tequila shots,” this crypto thing started to sound like possibly world-changing technology. Or total bullshit. The twins set out to research this crypto thing in detail, all across the world. The book chronicles their meetups and wild adventures with some of the biggest names in early Bitcoin. Remember, too, that this was the early Wild West days of Bitcoin, and there were some unbelievable characters involved in the crypto space. Stories of Charlie Shrem, Roger Ver, Ross Ulbricht and the infamous Silk Road site are great entertainment. Parties, drugs, concerts, you name it.

Finally, after doing their due diligence, there was nothing left to do with this Bitcoin thing but to make a bet. A big bet. And that they did. How much Bitcoin they own now is not publicly known, but they have acknowledged that they became “Bitcoin Billionaires” from their investment. They also founded the Gemini cryptocurrency exchange and have funded several start-up ventures. Mark Zuckerberg is one of the richest people in the world right now, but Tyler and Cameron’s “second act” had to be a satisfying dose of revenge and redemption following the Facebook ordeal.

Could Tyler and Cameron Winklevoss be at the center of another game-changing technology? Social media and digital money? At this point, with Bitcoin twelve years old and gaining acceptance every day, it certainly seems so. I highly recommend this book. It’s all at once wild, hysterical, suspenseful and informative. Every Bitcoiner should give it a read.

Oh, and here’s where Ben, Cameron and Tyler so graciously signed my book after I met them in New York:

This Week in Bitcoin History:

May 15, 2013: The crypto exchange Mt. Gox was slapped with a warrant from the US Department of Homeland Security, claiming that Mt. Gox operated as an unregistered money transmitter. The exchange, based in Japan, was at the time processing over 70% of the world’s Bitcoin trades. It was also hit with a plethora of other charges by regulators around the world. It was estimated that 850,000 Bitcoins had vanished from customer accounts. Mt. Gox filed for bankruptcy in 2015, in several countries. “Mt Gox” is still a dirty word in Bitcoin circles.

May 17, 2013: The first Bitcoin conference was held in San Jose, California. Tyler and Cameron Winklevoss, the Bitcoin Billionaires, were among the speakers. The conference drew only 1,000 attendees. The trade show booth for Coinbase was manned by just one person, CEO Brian Armstrong. How far we’ve come!

May 10, 2017: Yours truly inexplicably sold Bitcoins. At $1,800 each. Yeah, I don’t know what my thought process was. Therapy is going well, however.

Issue No. 2 May 14, 2021

Rick Mulvey is a CPA, forensic accountant and crypto consultant. He writes about all things Bitcoin, runs marathons, yells at the Yankees and Giants, and tries to make homemade wine.

Follow on Twitter! The Bitcoin Files Newsletter